|

|

|

|

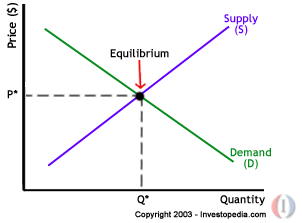

Market equilibrium is established when quantity supplied is equal to quantity demanded

At this point, the market sets the price (P) and quantity (Q) for a good or service

When equilibrium is established, both consumers and producers are made happy

|

|

|

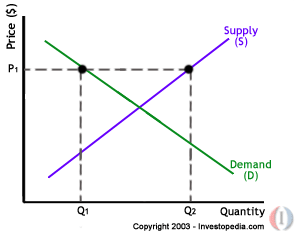

SURPLUS

quantity supplied > quantity demanded

there is relatively low demand, or a severe increase in supply

prices should naturally fall to cover these changes

|

|

|

|

|

|

|

|

|

|

|

|

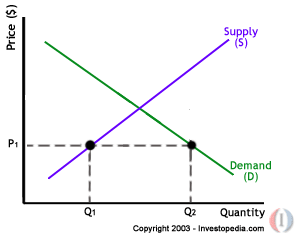

SHORTAGE

high demand, or low supply, also, price could

be lower than what the market would expect

the price should naturally increase due to cover these changes, aka the producer's

would raise prices due to high demand

Created Fall 2004

WFU '08

|

|

|

|